Currency exchange for a real estate purchase in Canada is the process of converting foreign funds into Canadian dollars to complete a property transaction, and how you handle it can determine whether you save or lose thousands. Most buyers focus on the property price and overlook the foreign exchange (FX) layer entirely. That is a costly mistake. Specialists like MTFX, Wise, and OFX charge spreads of 0.5–1% compared to the 2–4% markup typical of Canada’s Big 5 banks. On a $600,000 purchase, that difference alone can reach $13,440 CAD. Whether you are a Canadian buying abroad or an international buyer purchasing property in Canada, getting the currency conversion right is as important as negotiating the purchase price.

What are the best currency exchange options for buying property in Canada?

The standard industry term for this process is “foreign exchange” or FX, and the options available to buyers range from traditional bank wires to dedicated FX platforms built specifically for real estate transactions.

Traditional Canadian banks, including RBC, TD, Scotiabank, BMO, and CIBC, charge a 2–4% spread above the mid-market rate. That spread is embedded in the exchange rate itself, not listed as a separate fee. Most buyers never see it. On a $400,000 transfer, a 3% spread costs $12,000 CAD before any wire fees are added. That is money that disappears silently.

Specialised FX providers charge 0.5–1% spreads and often include dedicated real estate support teams. Providers like MTFX, Wise, and OFX are built for large, time-sensitive transfers. They understand closing deadlines, can coordinate directly with your lawyer’s trust account, and process wires faster than most bank channels. FX specialists save buyers $6,000–$13,440 CAD on large transfers compared to bank rates.

| Feature | Big 5 Banks | Specialised FX Providers |

|---|---|---|

| Exchange rate spread | 2–4% above mid-market | 0.5–1% above mid-market |

| Wire processing speed | 2–5 business days | 1–2 business days |

| Real estate support | General customer service | Dedicated real estate teams |

| Transparency of fees | Spread hidden in rate | Fees disclosed upfront |

| Forward contracts | Limited availability | Standard offering |

Forward contracts are one of the most useful tools available to property buyers. They let you lock in today’s exchange rate for a closing date 30–90 days away. This protects your budget from rate swings during due diligence and the period between offer acceptance and closing.

Pro Tip: Always verify wire instructions by calling your lawyer’s office directly before sending any funds. Wire fraud targeting real estate transactions is a real and growing threat. Never rely solely on emailed instructions.

How do Canadian laws and taxes affect currency exchange for non-residents?

Canadian regulations add meaningful costs and compliance steps for international buyers. Understanding these rules before you transfer any funds is not optional.

The Prohibition on the Purchase of Residential Property by Non-Canadians Act restricts most foreign nationals from buying residential property in Canada until january 2027. Exemptions exist for certain work permit holders, international students, and properties in specific price ranges or locations. The foreign buyer rules in Ontario are detailed and carry serious financial consequences if ignored.

Provincial taxes add further cost for non-resident buyers:

- Ontario Non-Resident Speculation Tax (NRST): 25% of the purchase price for foreign nationals buying in designated areas, including the Greater Golden Horseshoe.

- British Columbia Additional Property Transfer Tax (APTT): 20% for foreign buyers purchasing in Metro Vancouver and other taxable regions.

- Federal Underused Housing Tax: An annual 1% tax on the assessed value of certain residential properties owned by non-Canadian owners.

These provincial speculation taxes apply on top of standard land transfer taxes and closing costs. A buyer subject to Ontario’s NRST on a $700,000 property owes an additional $175,000. That amount must be included in your currency conversion planning from day one.

Anti-money laundering (AML) and know your customer (KYC) requirements apply to every large transfer entering Canada. Your FX provider and your real estate lawyer are both legally required to verify the source of your funds. Proving source of funds is one of the biggest compliance hurdles international buyers face. Prepare bank statements, tax returns, sale proceeds documentation, or gift letters well in advance. Delays in producing this documentation can hold up your closing.

Buyers from countries with capital controls, such as China, face an additional layer of planning. Annual transfer limits imposed by home country regulators mean funds often need to move in multiple tranches over time. Capital controls require careful coordination across multiple transfers, each fully documented for Canadian AML compliance. Start this process months before your target closing date.

What budgeting and financing considerations apply to currency conversion?

Buyers consistently underestimate the total amount they need to convert. The purchase price is only the starting point.

Closing costs run 1.5–4% of the purchase price in Canada, covering land transfer taxes, legal fees, title insurance, and adjustments. Down payment requirements follow a tiered structure: 5% on the first $500,000, 10% on the portion between $500,000 and $1,500,000, and 20% on any amount above $1,500,000. A buyer purchasing a $900,000 property needs a minimum down payment of $65,000, plus closing costs of $13,500–$36,000. Every dollar of that must be converted and transferred on time.

Currency fluctuations between offer acceptance and closing can reduce your buying power by 3–5% over 30–90 days. On a $600,000 purchase, a 4% adverse move costs $24,000 CAD. That is not a theoretical risk. Exchange rates between the US dollar, British pound, Euro, and Canadian dollar move meaningfully over a 60-day closing window.

Forward contracts address this risk directly. You pay a deposit of 2–5% of the contract value to lock the rate today. The forward points adjustment reflects interest rate differentials between currencies and is typically small for CAD/USD pairs over 30–90 days. The result is a predictable budget with no exposure to rate swings during the transaction.

Pro Tip: Build a currency buffer of at least 2% above your calculated need. Rate movements, additional fees, and last-minute adjustments are common. Having extra converted funds available prevents scrambling at closing.

The difference between a spot transfer and a forward contract matters here. A spot transfer converts funds at today’s rate for immediate delivery, typically within two business days. A forward contract locks today’s rate for a future delivery date. Use spot transfers when you need funds immediately. Use forward contracts when your closing is more than two weeks away.

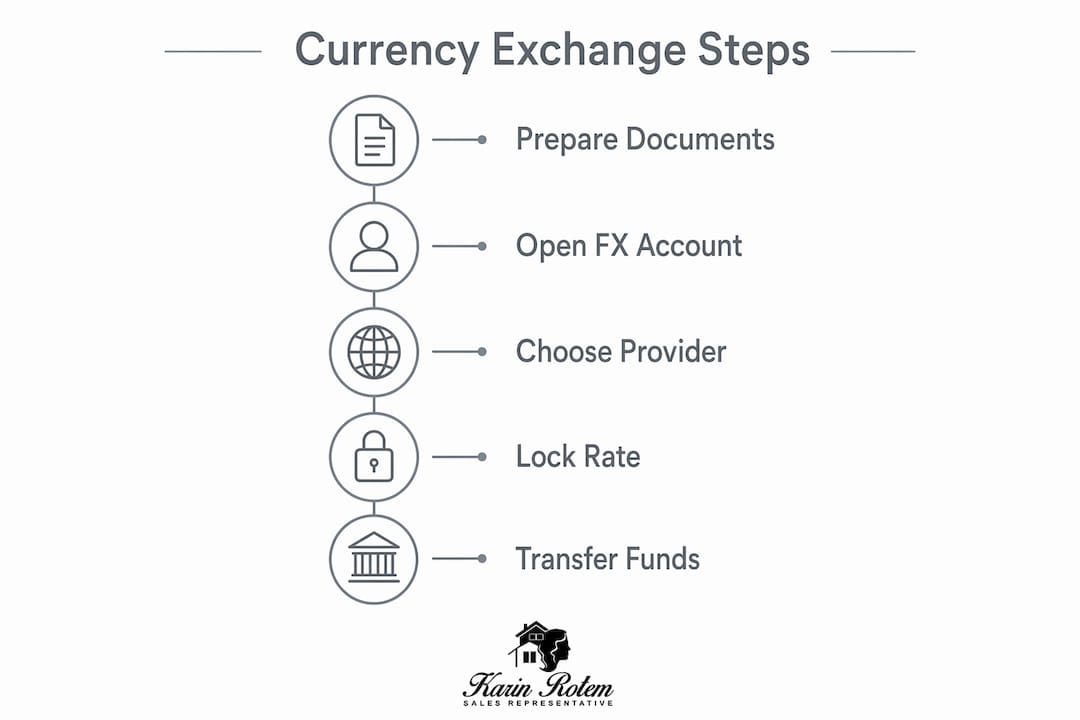

What is the step-by-step process to transfer funds for a Canadian property purchase?

A clear transfer process prevents the most common and costly mistakes buyers make.

-

Choose your FX provider early. Open an account with a specialised provider like MTFX, Wise, or OFX at least four weeks before your expected closing date. Complete identity verification and submit your source-of-funds documentation during this period, not the week before closing.

-

Calculate your total conversion need. Add the purchase price, closing costs (1.5–4%), applicable taxes (NRST or APTT if relevant), and a 2% contingency buffer. This is the total amount you need in Canadian dollars on closing day.

-

Decide between spot and forward. If your closing is more than two weeks away, a forward contract protects your budget. If you need funds within two business days, a spot transfer is appropriate. Discuss both options with your FX provider before committing.

-

Place your currency order. Confirm the exact amount, the delivery date, and the destination wire details with your provider. Your lawyer’s trust account details must be verified independently before this step.

-

Schedule the wire transfer early. AML holds on large bank wires can delay funds by days. Initiate your transfer at least three to five business days before the closing date to absorb any compliance review delays.

-

Confirm receipt with your lawyer. Follow up directly with your real estate lawyer to confirm funds have arrived in trust before closing day. Do not assume the transfer completed successfully without confirmation.

The most common pitfall is waiting too long. Buyers who initiate transfers the day before closing regularly face delays, holds, and in some cases, failed closings. Real estate deadlines are firm. A missed closing can cost you your deposit and expose you to legal liability.

Key takeaways

Specialised FX providers consistently outperform banks on cost, speed, and reliability for real estate currency transfers in Canada.

| Point | Details |

|---|---|

| Use FX specialists, not banks | Specialists charge 0.5–1% spreads versus 2–4% at banks, saving thousands on large transfers. |

| Budget beyond the purchase price | Add closing costs of 1.5–4%, applicable taxes, and a 2% buffer to your total conversion amount. |

| Lock rates with forward contracts | Forward contracts protect your budget from 3–5% currency swings during the 30–90 day closing window. |

| Prepare AML documentation early | Source-of-funds proof is legally required; delays in providing it can hold up your closing. |

| Verify wire instructions independently | Always call your lawyer directly to confirm wire details before sending any funds. |

What I tell every buyer about currency and closing day

What most buyers don’t realise is that the currency exchange decision is a financial decision, not an administrative one. I have worked with clients who saved more on their FX transfer than they saved through price negotiation. That is not an exaggeration.

The buyers who struggle are almost always the ones who treat the wire transfer as the last step. They focus entirely on the offer, the inspection, and the mortgage, and then scramble to move funds in the final week. That is when mistakes happen. Rates move. Wires get held for compliance review. Lawyers wait. Closings get complicated.

What I tell my clients is simple: treat the currency transfer as its own project with its own timeline. Open your FX account the same week you make your offer. Get your documentation together. Decide on a forward contract if your closing is more than two weeks out. Then you can focus on the property itself without a financial fire drill at the end.

The regulatory side matters too. International buyers who arrive without a clear understanding of Ontario’s NRST or the federal non-resident purchase restrictions sometimes face costs they were not prepared for. I always recommend reviewing the AML compliance requirements and the applicable tax rules before making an offer, not after. The total cost of ownership is what matters, and currency exchange is a meaningful part of that number.

— Karin Rotem

How Karinrotem supports buyers through the full purchase process

Karinrotem works with both Canadian and international buyers across Toronto, Innisfil, and the Friday Harbour community, where waterfront and lifestyle-driven properties attract buyers from across the country and around the world. The team provides guidance on foreign buyer rules, applicable taxes, closing cost planning, and the full property buying process in Canada. Whether you are purchasing a primary residence, a vacation property, or an income-generating investment, Karinrotem connects you with the right professionals at every stage. Browse current available properties and use the mortgage and affordability calculators for financial planning to build a clear picture of your total investment before you make an offer.

FAQ

What is the cheapest way to exchange currency for a Canadian property purchase?

Specialised FX providers like MTFX, Wise, and OFX charge 0.5–1% spreads compared to 2–4% at Canada’s Big 5 banks, making them the most cost-effective option for large real estate transfers.

Can non-residents buy property in Canada right now?

The Prohibition on the Purchase of Residential Property by Non-Canadians Act restricts most foreign nationals from buying residential property until january 2027, with exemptions for certain work permit holders and international students.

What taxes do foreign buyers pay when purchasing in Ontario?

Foreign buyers in Ontario pay the Non-Resident Speculation Tax at 25% of the purchase price in designated areas, in addition to standard land transfer taxes and closing costs.

How early should I start the currency transfer process?

Open your FX account and prepare your source-of-funds documentation at least four weeks before your expected closing date, and initiate the wire transfer three to five business days before closing.

What is a forward contract and do I need one?

A forward contract locks your exchange rate today for a closing date 30–90 days away, protecting your budget from currency swings that can reduce buying power by 3–5% over a typical transaction window.