A vacation home near Toronto is defined as a recreational or secondary property purchased within driving distance of the city, typically in areas like Kawartha Lakes, Muskoka, or Innisfil, offering owners a combination of personal enjoyment, rental income potential, and long-term asset growth. The question of why buy a vacation home near Toronto has a clear answer for many buyers: you get more space, direct access to nature, and a property that can generate income while you’re not using it. Victoria Preston, a buyer profiled by The Globe and Mail, purchased waterfront property in Kawartha Lakes in 2023 for roughly $700,000 and rents it most of the year, using that income to help finance her Toronto condo. That model is becoming a blueprint for a growing number of buyers who see cottage country not as a luxury, but as a practical path to ownership.

Why buy a vacation home near Toronto instead of city real estate?

The core appeal of buying a cottage near Toronto comes down to value, space, and flexibility. Waterfront properties in areas like Kawartha Lakes are priced comparably to Toronto condos but offer significantly more land, privacy, and rental income potential. For buyers priced out of Toronto’s urban market, this trade-off is increasingly attractive.

What I tell my clients is that the lifestyle shift alone often justifies the decision. A two-hour drive from Toronto puts you on a lake, in a forest, or at a resort community like Friday Harbour in Innisfil. That kind of access to nature, particularly for families with children, is genuinely difficult to replicate in a city condo. Remote work has made this even more practical, since many buyers now split their time between the city and their recreational property rather than treating it as a pure weekend retreat.

The buyer pool for Toronto weekend getaway homes has also broadened. Recreational properties serve as gateway assets and equity-building tools for younger Canadians who use rental income to offset carrying costs. This dual-use model, personal enjoyment combined with short-term rental revenue, is one of the strongest reasons to invest in vacation property near Toronto right now.

Here is what makes these locations stand out compared to city real estate:

- More land and privacy for the same price as a Toronto condo

- Direct waterfront or nature access within a two-hour drive of the city

- Lower competition in many cottage country markets compared to Toronto’s urban core

- Rental income potential through platforms like Airbnb and VRBO during peak seasons

- Lifestyle flexibility for remote workers who can use the property more than just on weekends

The advantages of owning a vacation home near Toronto extend beyond the financial. For many families, the property becomes a gathering place, a legacy asset, and a source of genuine wellbeing.

What are the real costs of owning a vacation property near Toronto?

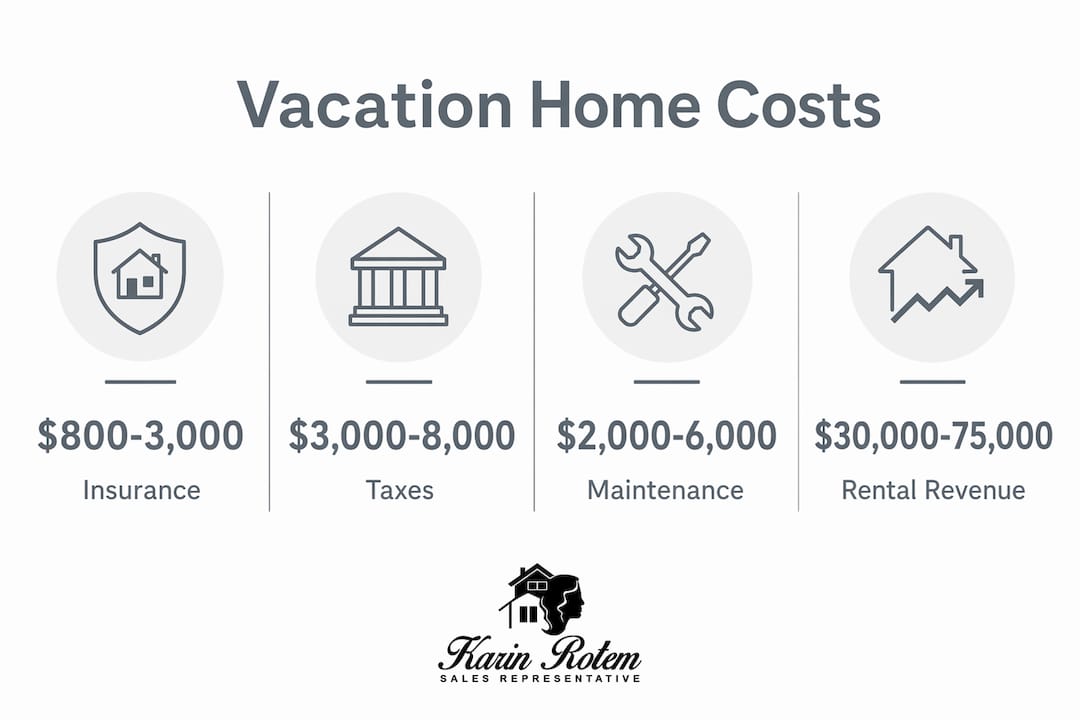

This is where honest planning separates confident buyers from regretful ones. The purchase price is only the beginning. What most buyers don’t realise is that year-round carrying costs, including insurance, property taxes, maintenance, and utilities, can collectively match or exceed mortgage payments if not budgeted carefully.

Here is a realistic breakdown of annual ownership costs you should plan for:

- Cottage insurance: Canadian premiums range from $800 to $3,000 annually, depending on remoteness, access, and hazard risk. A waterfront property on a private road will sit at the higher end of that range.

- Property taxes: Recreational properties are assessed differently by municipality. Budget $3,000 to $8,000 annually depending on location and assessed value.

- Maintenance and repairs: Septic systems, docks, roofing, and seasonal opening and closing costs add up. A conservative annual maintenance budget is 1% to 2% of the property’s value.

- Utilities: Hydro, water, heating, and internet for a property used year-round can add $4,000 to $8,000 annually.

- Mortgage carrying costs: A second property mortgage typically requires a minimum 20% down payment and carries a higher interest rate than a primary residence.

On the income side, gross rental revenue for well-located properties near Toronto typically ranges from $30,000 to $75,000 annually. Net income, after platform fees, cleaning, management, and vacancy periods, often covers only a portion of total carrying costs. Rental income provides financial confidence, but it should not be the sole reason you buy.

Pro Tip: Before purchasing, build a detailed cash-flow model that includes all five cost categories above. If the numbers only work with maximum rental occupancy, the property carries more financial risk than most buyers realise.

| Cost category | Estimated annual range |

|---|---|

| Cottage insurance | $800 to $3,000 |

| Property taxes | $3,000 to $8,000 |

| Maintenance and repairs | 1% to 2% of property value |

| Utilities | $4,000 to $8,000 |

| Gross rental income (offset) | $30,000 to $75,000 (before fees) |

Capital gains tax is another consideration that advisors frequently flag. Unlike a principal residence, a vacation property is fully subject to capital gains tax on sale. Estate planning implications, particularly for families passing properties to children, require early legal and tax advice. Clarifying your purchase intent, whether lifestyle, investment, or legacy, shapes every financial decision that follows.

How do local regulations affect renting out vacation homes near Toronto?

Short-term rental rules near Toronto vary significantly by municipality, and non-compliance carries real financial consequences. What I see most often is buyers who purchase with rental income in mind but underestimate the regulatory complexity before they list their first booking.

Key rules to understand before you rent:

- Muskoka Lakes: A by-law effective in 2026 requires summer rentals to block a minimum of seven consecutive nights per month and mandates at least $2 million in liability insurance. This significantly limits rental frequency during peak season, which is when nightly rates are highest.

- HST registration: In Ontario, short-term rental income is subject to 13% HST. Once your taxable revenue exceeds $30,000 over four consecutive quarters, HST/GST registration becomes mandatory. Failing to register means you cannot claim input tax credits, which increases your net tax burden considerably.

- Municipal accommodation taxes: Many Ontario municipalities now levy a Municipal Accommodation Tax on short-term rentals. This is separate from HST and must be collected and remitted independently.

- Licensing requirements: Most municipalities require a short-term rental licence, annual renewal, and proof of insurance. Operating without one risks fines and the loss of your ability to deduct rental expenses.

Pro Tip: Register for HST proactively if you plan to rent, even before you hit the $30,000 threshold. This allows you to claim input tax credits on renovation and furnishing costs from day one, which can meaningfully reduce your tax exposure in the first year.

For a full walkthrough of Ontario’s rental rules, the Ontario short-term rental guide from Karinrotem covers licensing, tax registration, and compliance steps in detail.

How does buying a cottage near Toronto compare with a Toronto condo investment?

This is the comparison I walk through with almost every client who is weighing their options. Both asset types have merit, but they serve different goals and carry different risks.

The price point for a waterfront property in Kawartha Lakes or a resort community like Friday Harbour in Innisfil can be comparable to a Toronto condo, but the experience of ownership is fundamentally different. A Toronto condo offers urban convenience, lower maintenance responsibility, and a liquid resale market. A vacation property offers space, nature, rental income flexibility, and a lifestyle return that no condo can replicate.

On the investment side, vacation properties rarely yield returns that compete with diversified financial portfolios. Seasonal vacancy, management complexity, and regulatory compliance all reduce net income. Toronto condos carry their own risks, including condo fee increases, special assessments, and a softening resale market in 2025 and 2026. Neither option is a guaranteed winner.

| Factor | Vacation property near Toronto | Toronto condo |

|---|---|---|

| Purchase price | $600,000 to $1,200,000+ | $550,000 to $900,000+ |

| Rental income potential | Seasonal, $30,000 to $75,000 gross | Year-round, more predictable |

| Maintenance responsibility | High, owner-managed | Lower, shared via condo fees |

| Lifestyle value | High, nature and recreation | Moderate, urban convenience |

| Regulatory complexity | High, municipal licensing required | Lower, standard tenancy rules |

| Capital gains on sale | Fully taxable | Fully taxable (non-principal) |

What the table above makes clear is that the decision is not purely financial. If your goal is a reliable passive income stream with minimal management, a Toronto condo may suit you better. If your goal is a property your family will use and love, with rental income as a supplement rather than the primary return, a vacation property near Toronto offers something a condo simply cannot. You can explore the Innisfil vs Toronto comparison for a deeper look at how these markets differ in 2026.

For buyers considering second home financing, understanding the mortgage structure for recreational properties early in the process avoids surprises at the offer stage.

Key takeaways

Buying a vacation home near Toronto makes the most financial and personal sense when you treat it primarily as a lifestyle asset, plan carefully for carrying costs, and understand local rental regulations before you purchase.

| Point | Details |

|---|---|

| Location value | Kawartha Lakes and Innisfil offer waterfront access at prices comparable to Toronto condos. |

| True ownership costs | Annual carrying costs including insurance, taxes, and maintenance can match or exceed mortgage payments. |

| Rental income reality | Gross rental revenue of $30,000 to $75,000 is possible, but net income after fees often covers costs only partially. |

| Regulatory compliance | Ontario HST registration is mandatory above $30,000 revenue; Muskoka Lakes imposes strict 2026 rental restrictions. |

| Purchase intent clarity | Defining your goal as lifestyle, investment, or legacy shapes every financing and tax decision that follows. |

What I’ve learned from helping clients buy vacation homes near Toronto

After years of working with buyers across Toronto, Innisfil, and the Friday Harbour community, the pattern I see most often is this: buyers arrive excited about the lifestyle and underestimate the operational reality. That is not a reason to walk away. It is a reason to go in with clear eyes.

The clients who are happiest with their vacation properties are the ones who bought primarily because they wanted to use the property. Rental income gave them financial confidence, but it was never the whole plan. The clients who struggle are the ones who bought assuming rental revenue would cover everything, then discovered that a Muskoka by-law, a slow booking season, or an unexpected septic repair changed the numbers entirely.

What I always ask is this: if you never rented this property once, would you still want to own it? If the answer is yes, the finances are manageable, and the location fits your life, then the decision usually makes sense. If the answer depends entirely on rental income projections, I recommend revisiting the cash-flow model before signing anything.

Location choice matters more than most buyers expect. Proximity to amenities, road access in winter, and the specific municipal rules in your target area all affect both your enjoyment and your rental viability. Friday Harbour in Innisfil, for example, offers resort-level amenities, year-round access, and a well-established community, which makes it a very different ownership experience than a remote lakefront property two hours north.

— Karin Rotem

Find your ideal vacation property near Toronto with Karinrotem

If you are ready to move from considering to deciding, Karinrotem is here to help you find the right property with confidence. Our team specialises in waterfront and lifestyle-driven real estate across Toronto, Innisfil, and the Friday Harbour community, with deep knowledge of local market conditions, rental regulations, and financing realities in 2026. We work with first-time recreational buyers and seasoned investors alike, tailoring our guidance to your specific goals. Browse our current vacation home listings to see what is available right now, or explore the Friday Harbour resort guide to understand what resort community ownership looks like in practice. Reach out directly to start a conversation about what fits your life and your budget.

FAQ

Why buy a vacation home near Toronto rather than further away?

Properties within two hours of Toronto offer the best combination of personal accessibility and rental demand. Buyers can use the property on weekends without losing a full day to travel, and renters prefer locations they can reach easily from the city.

What is the minimum down payment for a vacation property in Ontario?

A second property in Ontario typically requires a minimum 20% down payment. Unlike a primary residence, vacation homes do not qualify for CMHC mortgage insurance, so lenders require a larger equity position upfront.

Do I need to charge HST on my cottage rental income?

Yes, once your short-term rental revenue exceeds $30,000 over four consecutive quarters, HST registration is mandatory in Ontario. You must collect and remit 13% HST on rental income and file returns accordingly.

Should I buy a cabin near Toronto as an investment or lifestyle property?

Advisors consistently recommend treating vacation homes as lifestyle assets first. Rental income can supplement costs, but properties that depend entirely on rental revenue to break even carry significant financial and operational risk.

What are the best locations for second homes near Toronto?

Kawartha Lakes, Innisfil, and the Muskoka region are the most popular areas for Toronto buyers. Each offers different price points, regulatory environments, and rental demand profiles, so the best choice depends on your budget, intended use, and distance preference.