A pre-construction condo is a residential unit purchased before or during the construction of the building, typically through a staged deposit paid over several years. Buyers sign a legally binding Agreement of Purchase and Sale (APS) and commit to a unit that does not yet exist. The appeal is real: you lock in today’s price, choose your finishes, and potentially benefit from price appreciation by the time the building completes. Regulatory bodies like the Condominium Authority of Ontario and Tarion Warranty Corporation provide buyer protections, but the process carries distinct financial and legal risks that every Canadian buyer needs to understand before signing.

How does the pre-construction condo buying process work?

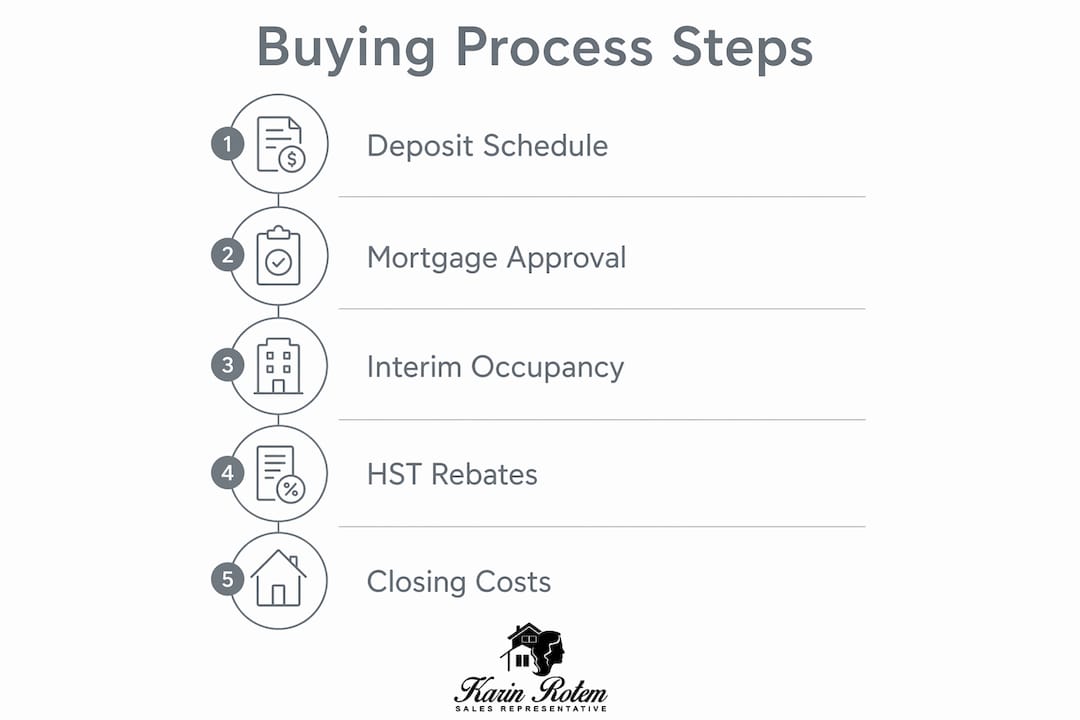

The pre-construction condo buying process follows a structured timeline that spans several years. Understanding each phase protects your deposit and your financial position.

-

Signing the Agreement of Purchase and Sale. You sign the APS and pay an initial deposit, typically 5% of the purchase price. This is the moment the contract becomes legally binding. Ontario law grants you a 10-day cooling-off period after receiving all disclosure documents, giving you time to have a real estate lawyer review the contract before you are fully committed.

-

Paying staggered deposits. Pre-construction condo deposits total 15%–20% of the purchase price, paid in instalments over 12–24 months. A common structure might be 5% at signing, 5% at six months, and the remainder at 12 months. This spread helps cash flow compared to a single lump sum, but you must have the funds available on each due date regardless of market conditions.

-

The construction period. Building timelines typically run two to five years from the date of signing. Delays are common. Developers are permitted to extend closing dates under the APS, sometimes by a year or more, which affects your mortgage planning and living arrangements.

-

Interim occupancy. Before the building receives its final registration, you may be permitted to move in and pay interim occupancy fees. These fees cover interest on the unpaid balance, property taxes, and maintenance costs. You are not yet the legal owner, and no equity is being built during this phase.

-

Final closing. The building registers with the municipality, your mortgage activates, and you take legal title. This is when you must requalify for your mortgage under current lending conditions, not the conditions that existed when you signed.

Pro Tip: Hire a real estate lawyer before the cooling-off period expires. A lawyer experienced in pre-construction contracts will identify problematic clauses around closing extensions, assignment rights, and deposit protection that a standard review would miss.

What are the benefits and risks of pre-construction condo investment?

Pre-construction condos offer genuine advantages, but the risks in 2026 are more pronounced than they were five years ago. A clear-eyed view of both sides is the only responsible way to approach this decision.

The real benefits

- Price appreciation potential. If market values rise between signing and closing, you gain equity before you take possession. Buyers who signed in 2017 and closed in 2020 in Toronto experienced this firsthand.

- Customisation options. Many developers allow buyers to select finishes, flooring, and cabinetry during a design appointment. This is not available with resale properties.

- Staggered deposits. Spreading payments over 12–24 months gives you time to save rather than requiring a large lump sum at once.

- New building warranties. Tarion Warranty Corporation covers structural defects and deposit protection for Ontario buyers, providing a layer of security that resale purchases do not include.

- Modern amenities. New buildings often include luxury amenity packages that older resale stock cannot match.

The significant risks in 2026

“The deciding factor for a safe pre-construction purchase is buyer liquidity and stress test qualification, not the project quality itself.” — Mortgage expert Razi Khan

- Appraisal gaps. Appraisal gaps have increased significantly in 2026 for units bought at peak 2021–2022 pricing. If your unit appraises below the purchase price at closing, your lender will not cover the difference. You pay it out of pocket or risk losing your deposit.

- Maintenance fee escalations. Condo maintenance fees can rise 30%–50% after the first year of occupancy. Investors who modelled cash flow on the developer’s initial estimates often find the numbers no longer work.

- Construction delays and cancellations. Projects can be delayed by years or cancelled outright. Tarion provides deposit protection in cancellation scenarios, but you lose years of opportunity cost.

- Legal consequences of failing to close. Pre-construction contracts are legally binding, and failure to close can result in lawsuits and full deposit forfeiture. There is no easy exit once the cooling-off period passes.

What financial considerations matter most for pre-construction buyers?

The financial complexity of buying pre-construction is greater than most buyers expect. These are the factors that determine whether the purchase works in your favour.

Mortgage qualification at closing

Mortgage pre-approval at signing does not guarantee final qualification. Buyers must requalify at closing under current financial conditions, including updated stress tests and interest rates. If rates have risen or your income situation has changed, you may not qualify for the mortgage you planned on. The consequence is deposit forfeiture and potential legal action.

The OSFI stress test

The Office of the Superintendent of Financial Institutions (OSFI) stress test requires buyers to qualify at their contract rate plus 2%. This buffer exists to protect buyers from rate increases, but it also reduces the mortgage amount you qualify for. Buyers with limited cash reserves should approach pre-construction with caution.

Interim occupancy fees

During the interim occupancy phase, phantom rent ranges from $2,000–$3,500+ monthly. You pay interest on the unpaid balance, property taxes, and maintenance fees. No principal is reduced. This phase can last several months and represents a real carrying cost that many buyers fail to budget for.

HST rebates and tax implications

| Buyer type | HST rebate eligibility | Key condition |

|---|---|---|

| Primary residence buyer | Up to $24,000 rebate | Must occupy as principal residence |

| Investor or rental buyer | Rebate may be repayable | Must assign rebate to developer or repay CRA |

| Assignment sale buyer | Varies by agreement | Legal and tax advice required |

The HST rebate structure rewards owner-occupants and penalises investors who do not plan properly. Speak with a tax professional before closing to understand your exact obligation.

Pro Tip: Budget a cash reserve of at least 5% above your deposit for appraisal gaps, closing costs, and interim occupancy fees. Buyers who enter pre-construction without this buffer are the ones who end up in trouble at closing.

Is a pre-construction condo the right choice for your goals?

Not every buyer is suited to pre-construction. The right fit depends on your financial position, investment horizon, and risk tolerance.

- Assess your liquidity. You need cash reserves beyond your deposit. Appraisal gaps, closing costs, and interim occupancy fees can add tens of thousands of dollars to your total outlay. If your savings are fully committed to the deposit, pre-construction is a high-risk move.

- Match your timeline to the project. Construction takes two to five years. If you need housing within 12 months, a resale property is the practical choice. Pre-construction suits buyers with flexibility and a long investment horizon.

- Engage a real estate lawyer early. Review the APS before the 10-day cooling-off period expires. Pay particular attention to clauses covering closing extensions, assignment rights, and what happens if the project is cancelled.

- Research the developer. A developer’s track record on past projects tells you more than any marketing brochure. Look at their history of on-time delivery, quality of construction, and how they handled disputes.

- Evaluate the location critically. Markets like Friday Harbour condos illustrate how location-specific factors, including waterfront access, resort amenities, and proximity to Toronto, shape both the risks and the upside of a pre-construction purchase.

- Consider resale as an alternative. Resale condos offer immediate possession, known maintenance fees, and a status certificate that reveals the building’s financial health. For buyers who cannot absorb the uncertainty of a multi-year construction timeline, resale is often the safer path.

Key takeaways

A pre-construction condo suits buyers with strong liquidity, a long investment horizon, and professional legal and mortgage guidance in place before signing.

| Point | Details |

|---|---|

| Deposits are staggered | Total 15%–20% of purchase price, paid over 12–24 months, not all upfront. |

| Mortgage approval is not guaranteed | You must requalify at closing under current stress test rules, not conditions at signing. |

| Interim occupancy costs are real | Phantom rent of $2,000–$3,500+ monthly builds no equity during this phase. |

| Maintenance fees rise sharply | Budget for increases of 30%–50% after the first year of occupancy. |

| Legal exit is not easy | Failing to close on a binding APS risks full deposit loss and potential lawsuits. |

What I’ve learned from watching buyers navigate pre-construction

Pre-construction condos are not inherently good or bad investments. They are a tool, and like any tool, the outcome depends entirely on how prepared the person using it is.

What I see most often is buyers who focus on the excitement of a new building and the promise of price appreciation, and who underestimate the financial endurance required to get to closing. The cooling-off period is ten days. That is not much time to have a lawyer review a contract, consult a mortgage broker about stress test qualification, and honestly assess whether your cash reserves can absorb an appraisal gap.

The buyers I have seen do well with pre-construction share three traits: they had cash reserves well beyond their deposit, they worked with a mortgage broker from day one rather than assuming their pre-approval would hold, and they chose developers with a proven track record. The buyers who struggled were often the ones who stretched to get into a project at peak pricing and then faced a market correction before closing.

Friday Harbour is a market I know well, and it illustrates the point clearly. The lifestyle appeal is genuine. But the risks of buying a condo in any resort or waterfront community are amplified when you add pre-construction timelines to the equation. My honest advice: if you are not in a position to close even if the market softens, do not sign.

— Karin Rotem

Working with Karinrotem on your pre-construction purchase

Pre-construction decisions carry real financial weight, and the right guidance from the start makes a measurable difference. Karinrotem works with buyers and investors across Toronto and Friday Harbour, providing honest, experience-based advice on whether a specific project fits your goals and financial position. The team helps you assess developer track records, review APS terms with the right professionals, and plan for the carrying costs that catch most buyers off guard. If you are ready to explore current listings or want a frank conversation about whether pre-construction suits your situation, Karinrotem is the place to start. Visit karinrotem.com to connect with the team directly.

FAQ

What is a pre-construction condo in Canada?

A pre-construction condo is a unit purchased before or during the construction of the building, with the buyer signing a legally binding APS and paying deposits in instalments over 12–24 months before taking possession.

How long does a pre-construction condo take to complete?

Construction timelines typically run two to five years from the date of signing, and developers are legally permitted to extend closing dates under the terms of the APS.

What is interim occupancy in a pre-construction condo?

Interim occupancy is the phase where buyers move into their unit before the building is legally registered. During this period, buyers pay monthly fees covering interest, taxes, and maintenance without building any equity.

Can I lose my deposit on a pre-construction condo?

Yes. If you cannot close at the final date, you risk forfeiting your full deposit. Tarion Warranty Corporation protects deposits if a developer cancels the project, but buyer-initiated failures to close are not covered.

Is the HST rebate available on pre-construction condos?

Primary residence buyers can receive an HST rebate of up to $24,000. Investors who do not occupy the unit as a principal residence may be required to repay the rebate to the Canada Revenue Agency.

Recommended

- What is a condo hotel unit? Your Canadian buyer’s guide

- Luxury condo amenities explained: Ontario buyer’s guide

- How to Buy a Friday Harbour Condo in 2025 | A Step-by-Step Buyer’s Guide – Karin Rotem Real Estate Agent

- Are There Pre-Construction Condos at Friday Harbour? | What Buyers Need to Know – Karin Rotem Real Estate Agent