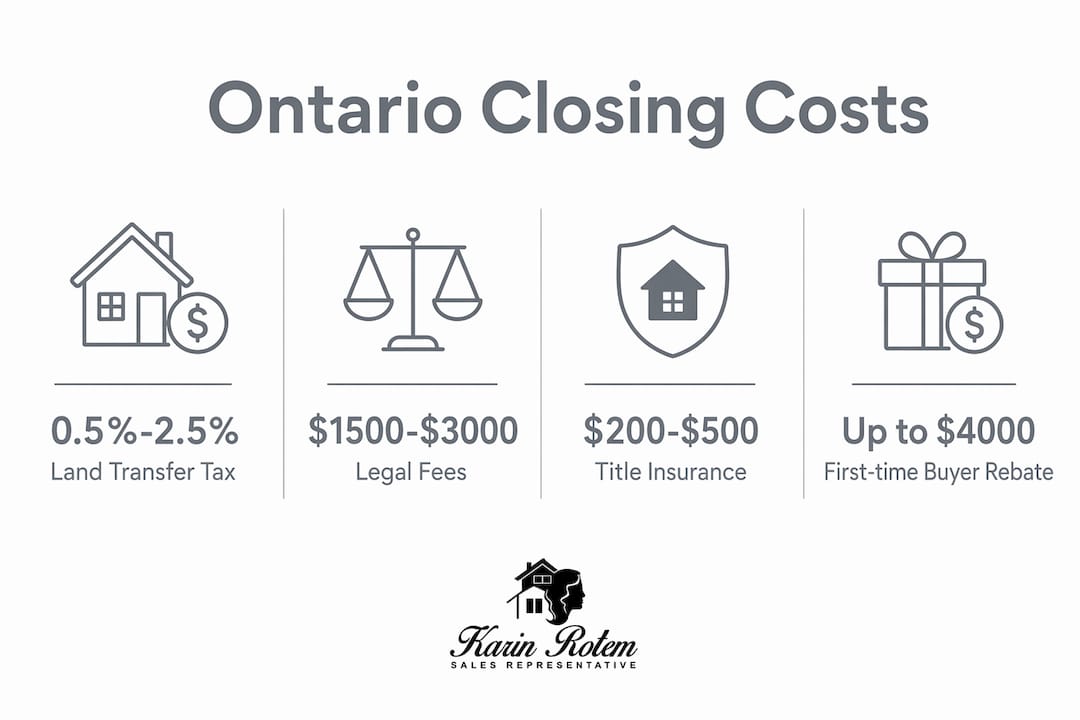

Closing costs in Ontario are the fees and charges a buyer must pay on top of the purchase price to complete a property transaction. These costs cover land transfer taxes, legal fees, title insurance, and a range of adjustments and disbursements. Buyers should budget between 1.5% and 4% of the purchase price for these expenses. On a $700,000 home, that means setting aside $10,500 to $28,000 in addition to your down payment. Understanding what closing costs include in Ontario before you sign anything is the single best way to avoid a stressful surprise on closing day.

What are the main components of closing costs in Ontario?

Ontario closing costs fall into several distinct categories. Each one is mandatory or near-mandatory, and each one requires cash on closing day.

Ontario Land Transfer Tax

The Ontario Land Transfer Tax (LTT) is the largest single closing cost for most buyers. It applies to every property purchase in the province and is calculated on a graduated, marginal basis. Toronto buyers also pay a Municipal Land Transfer Tax (MLTT) on top of the provincial amount. The LTT rates range from 0.5% to 2.5% depending on the purchase price bracket. That is a significant cost that catches many buyers off guard, especially in higher-priced markets like Toronto or Innisfil’s Friday Harbour.

Legal fees and disbursements

Every Ontario buyer needs a real estate lawyer. Legal fees typically range from $1,500 to $3,000, including disbursements and HST. Your lawyer handles the title search, document preparation, mortgage registration, and the actual transfer of ownership. Disbursements are the out-of-pocket costs your lawyer incurs on your behalf, such as government registration fees and courier charges. Always ask for a written estimate before retaining a lawyer so you know exactly what is included.

Title insurance

Title insurance costs between $200 and $500 and protects you against title defects, survey issues, and certain types of fraud. Lenders require a lender policy as a condition of mortgage funding in Ontario. Most buyers also purchase an owner’s policy, which protects their own equity. The cost is a one-time premium paid at closing, and the coverage lasts as long as you own the property.

Summary of typical Ontario closing costs

| Cost Item | Typical Range |

|---|---|

| Ontario Land Transfer Tax | Varies by price bracket (0.5%–2.5%) |

| Toronto Municipal Land Transfer Tax | Mirrors provincial rates for Toronto buyers |

| Legal fees and disbursements | $1,500–$3,000 (including HST) |

| Title insurance | $200–$500 |

| Home inspection | $400–$600 |

| Property tax adjustment | Varies by closing date |

| Mortgage default insurance PST | 8% of the insurance premium |

Pro Tip: Ask your lawyer for a full written estimate of all fees and disbursements before you sign a retainer. A good lawyer will itemise every line, and that document becomes your closing cost planning tool.

How is Ontario Land Transfer Tax calculated and what rebates exist?

The Ontario LTT uses a marginal bracket system, similar to income tax. Each portion of the purchase price is taxed at a different rate. Here is how the brackets work for a standard residential purchase:

- 0.5% on the first $55,000 of the purchase price.

- 1.0% on the portion between $55,001 and $250,000.

- 1.5% on the portion between $250,001 and $400,000.

- 2.0% on the portion between $400,001 and $2,000,000.

- 2.5% on any amount above $2,000,000.

Toronto buyers pay a second, parallel MLTT at the same bracketed rates. On a $700,000 Toronto home, a buyer pays both the provincial and municipal tax, which together can exceed $20,000. You can use the LTT affordability calculator on the Karinrotem website to run your own numbers before making an offer.

First-time buyer rebates

First-time buyers receive meaningful relief. The provincial rebate covers up to $4,000 of the Ontario LTT. Toronto’s MLTT rebate covers up to $4,475. To qualify, you must never have owned a home anywhere in the world, and you must occupy the property as your principal residence. Your lawyer applies for both rebates on your behalf at closing. The rebates are credited directly against your LTT owing, so you never pay the full amount and then wait for a refund.

| Rebate | Maximum Amount | Who Qualifies |

|---|---|---|

| Ontario LTT first-time buyer rebate | $4,000 | First-time buyers, principal residence |

| Toronto MLTT first-time buyer rebate | $4,475 | First-time buyers purchasing in Toronto |

For a detailed walkthrough of how the tax is calculated and paid, the Karinrotem guide on Ontario Land Transfer Tax covers every bracket with worked examples.

What are legal fees, title insurance, and other fixed closing costs?

Fixed closing costs are the ones you can confirm in advance with a phone call or email to your lawyer. They do not change based on your closing date or the seller’s tax situation.

- Legal fees: Cover the full scope of your lawyer’s work, including title search, document preparation, mortgage registration, and the transfer itself. Standard fees range from $1,500 to $3,000, inclusive of HST and disbursements.

- Title insurance (lender policy): Required by your mortgage lender. Protects the lender’s interest against title defects.

- Title insurance (owner’s policy): Protects your own equity. Strongly recommended even when not mandatory.

- Home inspection: Typically $400–$600. Not legally required, but skipping it is a risk most experienced buyers would not take.

- HST on legal fees: HST applies to your lawyer’s professional fees. It is included in most quoted ranges, but confirm this when you receive your estimate.

Pro Tip: When you get a quote from a lawyer, ask specifically whether the quoted amount includes HST and all disbursements. Some lawyers quote the professional fee only, which can make the final invoice feel much higher than expected.

Condo-specific closing costs include additional items like status certificate review fees and reserve fund adjustments, which are worth understanding if you are buying in a community like Friday Harbour.

What are the common adjustments and additional costs to prepare for at closing?

Adjustments are the variable costs that change based on your specific closing date and the seller’s prepaid expenses. These are calculated in the Statement of Adjustments, which your lawyer prepares before closing.

The Statement of Adjustments is the document that determines the exact amount you owe on closing day. It itemises the purchase price, your deposit, and every prorated cost. Most buyers see this document for the first time just days before closing, which is why early budgeting matters so much.

Property tax adjustments

Property tax adjustments can range from a few hundred to several thousand dollars depending on when you close and how far ahead the seller has paid. If the seller paid property taxes through june 30 and you close on may 1, you reimburse the seller for the two months of taxes they prepaid on your behalf. The reverse is also possible: if the seller has not yet paid taxes for the period before closing, they owe you a credit. The timing of your closing date directly affects this number.

Mortgage default insurance PST

If your down payment is less than 20%, you pay mortgage default insurance through Canada Mortgage and Housing Corporation (CMHC) or a private insurer. The premium itself is added to your mortgage. However, Ontario charges an 8% provincial sales tax on the insurance premium, and that PST must be paid in cash at closing. On a $10,000 premium, the PST is $800. That $800 cannot be rolled into your mortgage.

Other variable costs

- Utility adjustments: If the seller prepaid oil, propane, or other fuels, you reimburse them for the unused portion.

- Condo fee adjustments: If the seller prepaid condo maintenance fees, you credit them at closing.

- Appraisal fee: Your lender may require an independent appraisal, typically $300–$500, paid by you.

Closing costs must be paid in cash, usually by bank draft, on closing day. Failing to have these funds available can breach your Purchase Agreement. This is not a technicality. It is a contractual obligation with real legal consequences.

Pro Tip: Have your closing funds in a single account at least five business days before closing. Wire transfers and inter-bank moves can take longer than expected, and your lawyer needs certified funds, not a promise.

Key takeaways

Ontario closing costs are mandatory, cash-payable expenses that typically add 1.5%–4% to the total cost of buying a home, and every buyer must plan for them before making an offer.

| Point | Details |

|---|---|

| Budget 1.5%–4% above purchase price | On a $700,000 home, closing costs range from $10,500 to $28,000. |

| Land Transfer Tax is the largest cost | Ontario LTT uses marginal brackets from 0.5% to 2.5%; Toronto buyers pay a second municipal tax. |

| First-time buyers get rebates | Provincial rebate up to $4,000; Toronto MLTT rebate up to $4,475 for qualifying buyers. |

| All closing costs require cash | Funds must be available by bank draft on closing day; missing them can breach the Purchase Agreement. |

| The Statement of Adjustments is your final bill | This document itemises every prorated cost and determines the exact amount due at closing. |

What I tell every buyer about closing costs before they make an offer

What most buyers do not realise is that the Statement of Adjustments is not just paperwork. It is the document that tells you, sometimes 48 hours before closing, exactly how much money you need to hand over. I have seen buyers scramble to move funds at the last minute because they budgeted for the purchase price and the down payment but forgot that the seller prepaid six months of property taxes.

New builds carry a different set of risks. The 2026 temporary enhanced HST rebate for new home buyers can reduce closing costs significantly for qualifying properties up to $1 million. But new builds also come with development levies, utility connection fees, and Tarion warranty enrolment costs that resale purchases do not. Buyers who compare a resale quote to a new build quote without accounting for these extras often underestimate the gap.

My advice is always the same: get a written estimate from your lawyer before you firm up your offer, not after. Final closing costs are highly individualized, and a good lawyer will walk you through every line before you are committed. That conversation costs nothing and can save you thousands in stress and last-minute scrambling.

— Felix

Karinrotem can help you plan your Ontario closing costs

Buying property in Ontario involves more moving parts than most buyers expect, and closing costs are where the surprises tend to land. The Karinrotem team works with first-time buyers, seasoned investors, and everyone in between across Toronto, Innisfil, and Friday Harbour. We help you understand every cost before you make an offer, so there are no shocks on closing day. Whether you are buying a primary residence, a waterfront retreat, or an income property, we give you a clear picture of what you will actually pay. Visit Karinrotem’s real estate services to connect with our team and get guidance tailored to your situation.

FAQ

What does closing costs include in Ontario?

Ontario closing costs include the Land Transfer Tax, legal fees and disbursements, title insurance, property tax adjustments, and, where applicable, the PST on mortgage default insurance premiums. Buyers should budget 1.5%–4% of the purchase price for these expenses.

How much is the Ontario Land Transfer Tax on a $700,000 home?

The Ontario LTT on a $700,000 home is calculated using marginal brackets ranging from 0.5% to 2.5%. Toronto buyers also pay a Municipal Land Transfer Tax at the same bracketed rates, which can push the combined total well above $10,000.

Do first-time buyers get a rebate on closing costs in Ontario?

First-time buyers receive a provincial LTT rebate of up to $4,000 and, if purchasing in Toronto, a Municipal LTT rebate of up to $4,475. Your lawyer applies for both rebates automatically at closing.

Can closing costs be added to my mortgage in Ontario?

Closing costs generally cannot be rolled into your mortgage. The mortgage default insurance premium itself is added to the mortgage, but the 8% Ontario PST on that premium must be paid in cash at closing.

What is the Statement of Adjustments in Ontario real estate?

The Statement of Adjustments is a document your lawyer prepares before closing that itemises the final purchase price, your deposit, and all prorated costs such as property taxes and condo fees. It determines the exact cash amount you must deliver on closing day.