A rental income projection is a data-driven forecast of the revenue a rental property is expected to generate over a defined period, factoring in market rents, vacancy rates, and operating expenses. In the industry, you will also hear this called a pro forma analysis or a rental property forecast. Whether you are evaluating a condo at Friday Harbour, a Toronto investment property, or a furnished vacation unit in Innisfil, this forecast is the foundation of every sound investment decision. It tells you whether a property can actually pay for itself, and by how much. Without one, you are guessing.

What is a rental income projection and why does it matter?

A rental income projection answers one question before you commit a single dollar: can this property generate enough income to justify the investment? Lenders require it. Appraisers rely on it. And any investor who skips it is taking on risk they have not measured.

The projection typically includes four core components: market rental rates for comparable properties, a vacancy allowance to account for periods without tenants, operating expenses such as property management and maintenance, and a multi-year outlook that models rent increases of 2 to 5% annually. Each component shapes the final number, and each one carries assumptions that need to be tested.

What I tell my clients is that the importance of rental income projections goes beyond number-crunching. A well-built projection reveals whether a property fits your financial goals before you are legally committed to buying it. It also gives you a credible document to bring to your mortgage broker or lender, which can directly affect your financing terms.

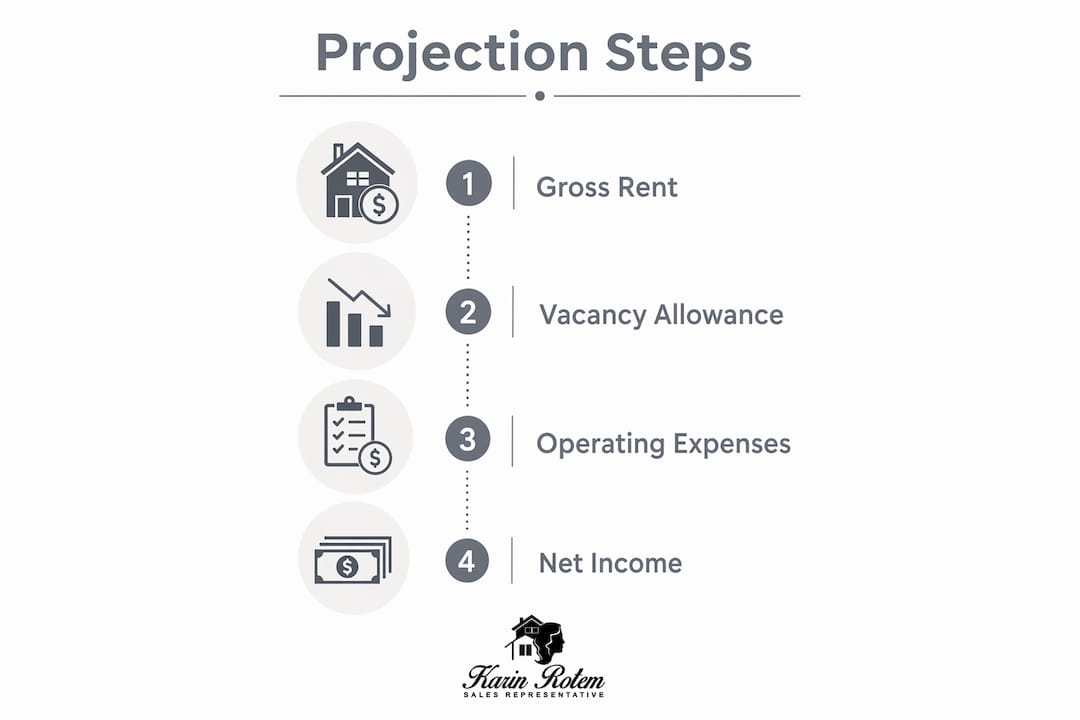

How to calculate rental income step by step

Calculating a rental income projection follows a clear sequence. Work through each step in order, and you will arrive at a number you can actually use.

-

Calculate Gross Potential Rent (GPR). Start by estimating the total rent the property would collect if it were occupied 100% of the time. Use current comparable listings in your target market to set this figure. For a two-bedroom condo at Friday Harbour, for example, you would research what similar units are renting for on both long-term and short-term platforms.

-

Apply a vacancy rate to find Effective Gross Income (EGI). No property stays fully occupied every month. Vacancy rates typically range from 5% to 12% depending on market strength and property type. A strong urban Toronto market might warrant a 5% vacancy assumption; a seasonal waterfront property in Innisfil might sit closer to 10 to 12%. Subtract your vacancy allowance from GPR to get EGI.

-

Subtract operating expenses. Operating expenses include maintenance at 10 to 15% of collected rent and property management fees at 8 to 12%. Add property taxes, insurance, condo maintenance fees, and any reserve fund contributions. These costs are not optional and they are rarely small.

-

Calculate Net Operating Income (NOI). NOI is EGI minus all operating expenses, before your mortgage payment. This is the number lenders and appraisers care about most.

-

Build a multi-year projection. Extend your model across three to five years, applying annual rent growth and modest expense increases. This reveals how the investment performs over time, not just in year one.

| Component | Typical range |

|---|---|

| Vacancy allowance | 5% to 12% of GPR |

| Property management fees | 8% to 12% of collected rent |

| Maintenance and repairs | 10% to 15% of collected rent |

| Annual rent growth assumption | 2% to 5% per year |

Pro Tip: Build your projection in a simple spreadsheet with three columns: conservative, moderate, and aggressive assumptions. Running all three scenarios side by side shows you the true risk range of the investment before you make an offer.

Common mistakes in rental income forecasting

Most projection errors come from optimism, not ignorance. Investors want a property to work, so they unconsciously shade their assumptions in its favour. The result is a forecast that looks great on paper and disappoints in practice.

The most common mistakes include:

- Assuming 0% vacancy. No property is occupied every single month, every single year. Using 100% occupancy in your model is not a projection. It is wishful thinking.

- Underestimating expenses. Many first-time investors forget capital expenditures entirely. A new roof, a replaced HVAC unit, or a kitchen refresh are not surprises. They are predictable costs that belong in your model.

- Confusing pro forma income with actual income. Pro forma rent is a projection based on market rates, not a guarantee. Treating it as certain income is one of the most costly errors in rental property analysis.

- Ignoring seasonality. Short-term rentals in markets like Friday Harbour are highly seasonal. A cottage that earns strong revenue in July and August may sit largely vacant in November. Your projection must reflect that reality.

- Overestimating rent. Most investors overestimate rental income by 10 to 15%, which can cut a projected 8% cash-on-cash return in half or push it into negative territory entirely.

“Treat projections as a hypothesis, not a guarantee. The goal is to stress-test your assumptions before the market does it for you.” — Bay Property Management Group

Pro Tip: When reviewing a short-term rental property, always ask for actual booking history rather than relying solely on projected income. Real occupancy data is far more reliable than optimistic estimates.

Gross rental income vs. net rental income: what is the difference?

Gross rental income is the total rent a property collects assuming full occupancy. It is the top-line number, and it is almost never the number that matters for investment decisions. Net rental income is what remains after you subtract all operating expenses from your effective gross income. That is the number that determines whether a property actually makes money.

Net Operating Income is the key profitability metric used by lenders and appraisers, not gross revenue. A property generating $36,000 per year in gross rent sounds attractive. But if operating expenses consume $22,000 of that, your NOI is $14,000. That is the figure your lender will use to assess debt serviceability, and it is the figure you should use to compare properties.

| Income type | What it includes | What it excludes |

|---|---|---|

| Gross Potential Rent | All rent at 100% occupancy | Vacancy, expenses, mortgage |

| Effective Gross Income | Rent minus vacancy allowance | Operating expenses, mortgage |

| Net Operating Income | EGI minus all operating expenses | Mortgage payments only |

The gap between gross and net income is where investment decisions are made or broken. A property with high gross rent but equally high expenses may underperform a more modest property with lower costs. What I always tell my clients is to compare properties on NOI, not on asking rent or headline revenue figures.

Pro Tip: Ask your accountant about deductible rental expenses including mortgage interest, property taxes, and depreciation. These deductions reduce your taxable income and improve your after-tax return, which changes the investment picture considerably.

Applying rental income projections to real investment decisions

A projection is only useful if you act on it. Here is how to put your rental income forecast to work at each stage of the investment process.

- Assessing cash flow feasibility. Before making an offer, calculate your projected NOI and subtract your estimated mortgage payment. If the result is positive, the property generates cash flow. If it is negative, you need to decide whether appreciation potential or other factors justify the shortfall.

- Financing applications. Lenders in Canada use NOI to assess whether a rental property can service its own debt. A well-prepared projection, built on realistic assumptions, strengthens your application and can improve the terms you receive.

- Setting rental rates. Your projection tells you the minimum rent you need to cover costs. Comparing that figure to current market rents tells you whether the property is viable at today’s prices or whether you are counting on future rent growth to make it work.

- Friday Harbour and Innisfil applications. For waterfront properties in the Friday Harbour community, rental income potential is shaped by seasonal demand, resort amenity fees, and the rental management programme offered on-site. A projection for a Friday Harbour condo must account for all of these variables, not just comparable market rents.

- Revisiting projections regularly. Rental income forecasting is an ongoing process, not a one-time exercise. Markets shift, expenses change, and interest rates move. Reviewing your projection annually keeps your investment strategy grounded in current reality rather than outdated assumptions.

For furnished investment properties, the features that drive rental demand directly affect your achievable rent and occupancy rate. A well-appointed unit commands a premium and reduces vacancy, both of which improve your projection materially.

Key takeaways

A rental income projection is only as reliable as the assumptions behind it, and conservative assumptions consistently outperform optimistic ones in real-world investment outcomes.

| Point | Details |

|---|---|

| Start with gross potential rent | Calculate total rent at 100% occupancy before applying any adjustments. |

| Always apply a vacancy rate | Use 5% to 12% depending on market strength to find realistic effective gross income. |

| NOI is the decision metric | Subtract all operating expenses from effective gross income to get the number lenders use. |

| Avoid pro forma overconfidence | Treat projected income as a hypothesis and stress-test with conservative, moderate, and aggressive scenarios. |

| Revisit projections annually | Market conditions, expenses, and rental rates change; update your model to stay accurate. |

What I have learned about projections after years in this market

The single biggest mistake I see investors make is treating a pro forma as a promise. A projection is a model. It is built on assumptions, and assumptions can be wrong. What separates experienced investors from first-timers is not the sophistication of their spreadsheets. It is their willingness to stress-test every number and ask what happens if rent comes in 10% lower or vacancy runs at 15% instead of 5%.

In the Friday Harbour market specifically, I have seen buyers get excited about peak-season rental income figures without accounting for the shoulder months. A condo that earns $4,500 in August may sit vacant for six weeks in the spring. Your annual projection needs to reflect the full twelve months, not the best three.

What I tell my clients is to build the conservative scenario first and make sure the investment still works at those numbers. If it only works under the optimistic scenario, that is not an investment. That is a bet. The most successful investors I work with in Toronto and Innisfil treat their projections as living documents, revisiting them every year and adjusting their strategy accordingly. That discipline is what turns a good property into a genuinely profitable one over time.

— Karin Rotem

Work with Karinrotem on your next investment property

Understanding rental income projections is one thing. Applying them to a specific property in a specific market is where the real work happens. At Karinrotem, we work with investors across Toronto and the Friday Harbour community to evaluate income-generating properties with clear financial analysis and local market knowledge. Whether you are assessing your first rental property or expanding an existing portfolio, we can help you build realistic projections and identify opportunities that align with your goals. Browse our current investment property listings to see what is available in the markets we know best, and reach out to start a conversation about your investment strategy.

FAQ

What is a rental income projection in real estate?

A rental income projection is a forecast of the revenue a rental property is expected to generate, accounting for market rents, vacancy rates, and operating expenses. It is used to evaluate investment feasibility, support financing applications, and guide financial planning.

How do you calculate rental income for an investment property?

Start with gross potential rent at 100% occupancy, subtract a vacancy allowance of 5 to 12%, then deduct operating expenses including management fees and maintenance to arrive at Net Operating Income.

What is a realistic vacancy rate to use in a projection?

Vacancy rates range from 5% in strong markets to 12% or higher for seasonal or high-end properties. Using a conservative rate prevents overstating projected income.

What is the difference between gross and net rental income?

Gross rental income is total rent collected assuming full occupancy. Net rental income, or NOI, subtracts all operating expenses and is the figure lenders and appraisers use to assess a property’s true profitability.

How often should I update my rental income projection?

Rental income forecasting is an ongoing process that should be revisited at least annually. Market rents, vacancy trends, and operating costs all shift over time, and your projection should reflect current conditions.

Recommended

- What is a short-term rental income property?

- How Does Rental Income Potential Work for Condos at Friday Harbour? – A Buyer’s Guide to Investment Returns – Karin Rotem Real Estate Agent

- Furnished rental property features investors need

- What’s the Average Rental Income at Friday Harbour? | Condo Investor Insights – Karin Rotem Real Estate Agent